Modernizing Defined Contribution Plans

Beyond traditional assets

The Challenge of the Traditional 60/40 Portfolio

For decades, the classic 60/40 portfolio—where 60% is allocated to stocks and 40% to bonds—has been the cornerstone of retirement investing. The idea was simple: when stocks were down, bonds would cushion the blow, and vice versa. It was a straightforward, effective approach that helped millions of investors grow their savings while managing risk.

But times have changed. Inflation, rising interest rates, geopolitical uncertainty, and evolving market dynamics have altered the effectiveness of this traditional model. Recent years has shown that bonds are no longer the reliable counterbalance they once were, particularly in environments where inflation remains stubbornly high. At the same time, evolving market dynamics has shifted many return seeking investments within both equity and fixed income into the private markets.

Rethinking Diversification: Introducing Alternative Investments

So, what’s the solution? Investors and plan sponsors should consider looking beyond traditional assets and incorporate alternative investments into their defined contribution (DC) plans. These alternatives—such as private equity, real estate, infrastructure, and private credit—offer the potential for higher returns, lower correlation to public markets, and better protection against inflation.

The Benefits of Alternative Investments

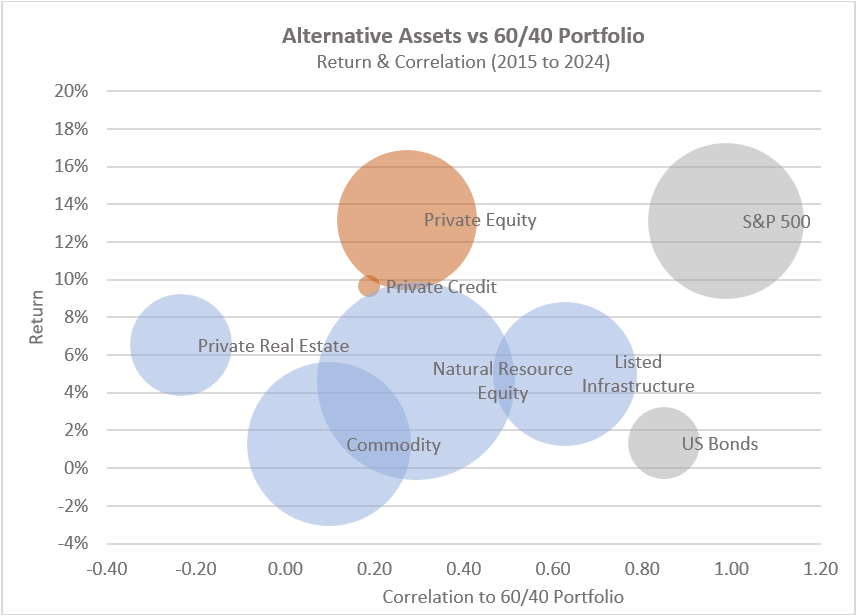

Enhanced Diversification: Traditional portfolios rely heavily on the stock-bond correlation. However, in recent years, that correlation has become less predictable. Alternatives provide exposure to asset classes that respond differently to economic shifts, adding resilience to portfolios.

Greater Return Potential: Historically, private equity has outperformed public markets over the long run. By gaining access to these private investments, DC plan participants can potentially achieve higher returns than through traditional public equities alone.

Source: eVestment

Inflation Protection: Assets like real estate and infrastructure have natural inflation-hedging characteristics. As inflation rises, the value of these investments tends to increase as well, providing a safeguard for investors who might otherwise see their purchasing power eroded.

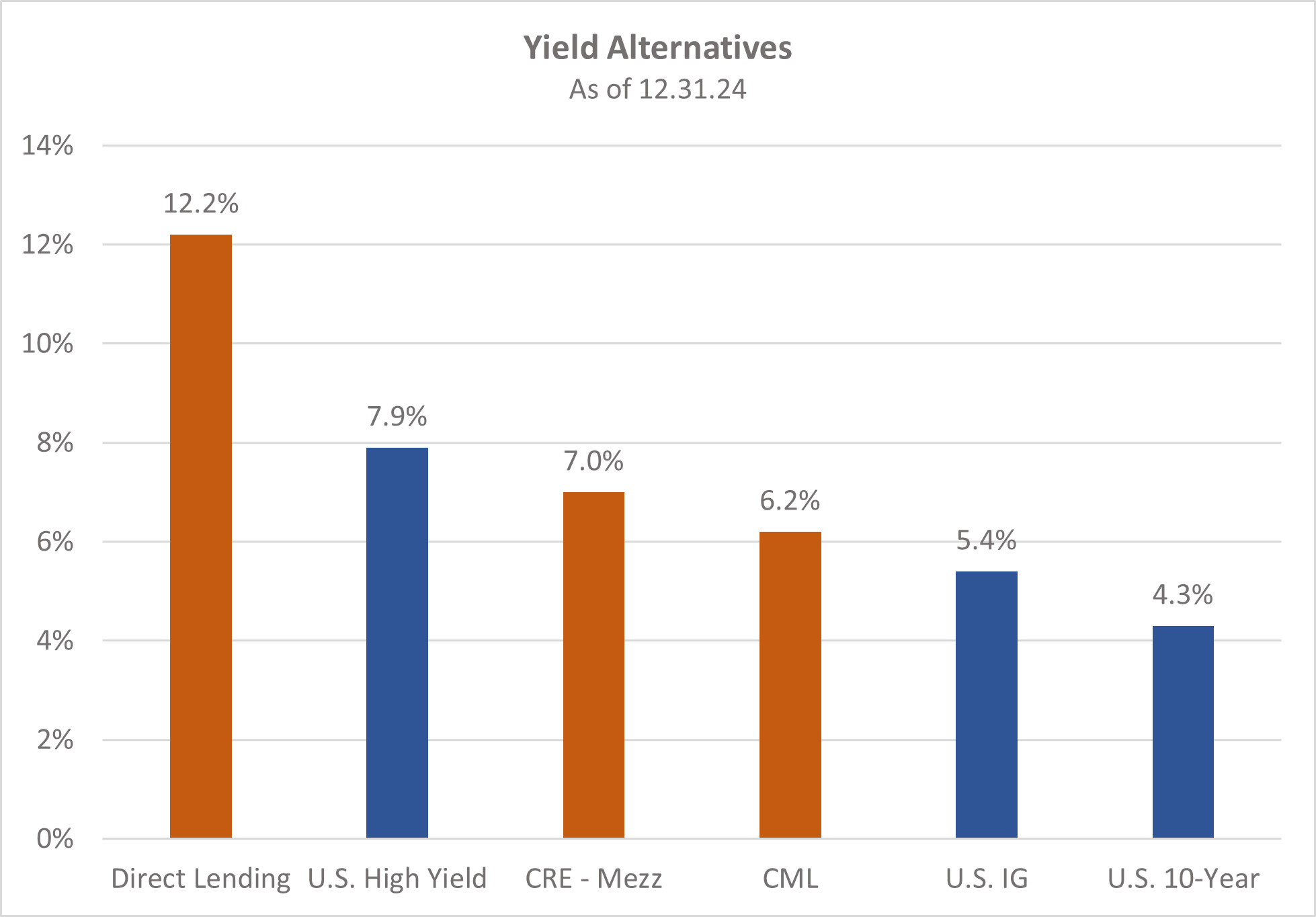

Income Generation: Private credit and direct lending offer attractive yield opportunities, especially in a high-interest-rate environment. Unlike traditional fixed income, which has struggled in recent years, private credit provides recurring cash flows and adjusts with interest rate changes.

Source: JP Morgan Asset Management. CRE – Mezz = mezzanine commercial real estate debt; CML = commercial mortgage loans

Reduced Volatility in Uncertain Markets: One of the biggest challenges for retirement savers is managing market volatility. Alternative investments, particularly those in private markets, tend to be less sensitive to short-term fluctuations in public markets. This stability can help investors stay committed to their long-term financial goals.

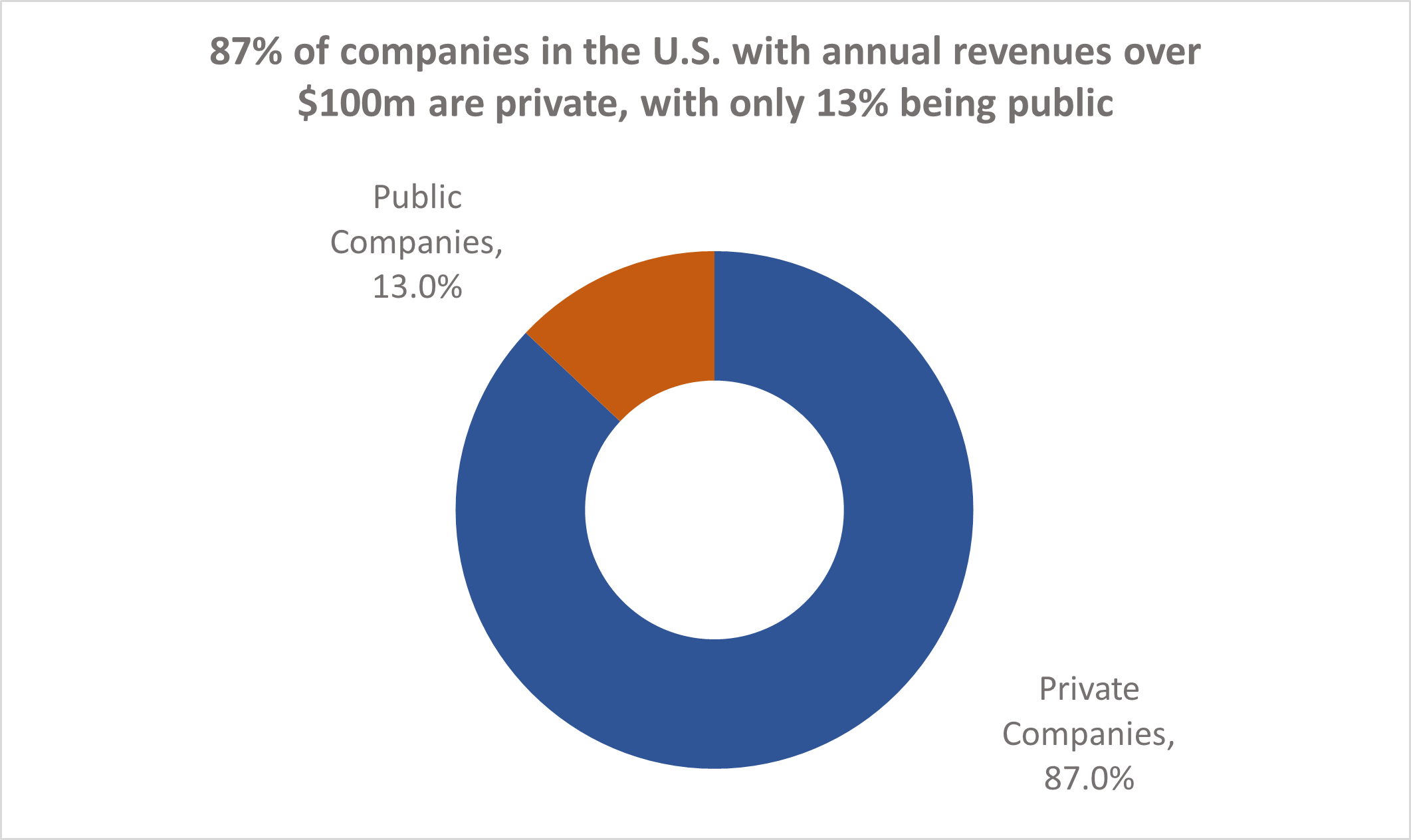

Expanded Opportunity Set: In recent years, traditionally public-bound companies have opted to stay private longer, driven by abundant private capital, regulatory scrutiny, and a desire to maintain strategic flexibility without the pressures of quarterly earnings reports. This is also happening on the debt side as banks have pulled back from traditional lending. More so than in years past, investors who ignore the private markets are missing out on a large portion of the investable universe and potential returns.

Source: Partners Group; Capital IQ. As of August 2023 (updated annually)

Overcoming the Barriers to Adoption

Despite their clear advantages, alternative investments have traditionally been underrepresented in DC plans due to several key hurdles. One major concern is liquidity. DC plans prioritize daily liquidity, whereas many alternative investments require longer lock-up periods. However, innovations such as semi-liquid funds and interval funds are helping to make these investments more accessible. Additionally, regulatory and fiduciary considerations pose challenges, as plan sponsors must ensure that alternative investments meet fiduciary standards and are suitable for a broad participant base. Fortunately, evolving regulations and new fund structures are addressing these concerns. Another significant challenge is operational complexity. Unlike traditional stocks and bonds, alternative investments often require more sophisticated management, valuation, and reporting. However, advancements in financial technology and investment platforms are streamlining these processes, making it easier for plan sponsors to incorporate alternatives into their offerings. Lastly, education and awareness remain a barrier, as many investors and plan sponsors are unfamiliar with alternative investments and their benefits. Expanding education efforts can help bridge this gap, enabling investors to better understand and embrace these opportunities.

Strategies for Integrating Alternatives into DC Plans

Successfully integrating alternative investments into DC plans requires a strategic and thoughtful approach. One effective strategy is incorporating alternative assets into target-date funds (TDFs), which are already a popular choice in DC plans. By embedding private equity, real estate, and private credit within these funds, participants can gain exposure to alternative investments without the need for direct management. Another approach is offering managed accounts that include alternative investments, allowing for personalized portfolio construction based on an individual’s risk tolerance and time horizon. Additionally, multi-asset funds that blend traditional and alternative assets can provide participants with diversified exposure while maintaining a straightforward investment structure. Lastly, educating plan participants about the benefits of alternative investments through seminars, webinars, and clear communication materials can enhance awareness, increase adoption rates, and improve overall investment outcomes.

The Future of Retirement Investing

As the investment landscape continues to evolve, so too must our approach to retirement savings. Defined contribution plans should no longer be limited to a rigid mix of stocks and bonds. By incorporating alternative investments, plan sponsors can help participants achieve better diversification, higher returns, and improved financial security in retirement.

The time for change is now. With thoughtful implementation, alternative investments can play a pivotal role in modernizing retirement plans, ensuring that investors are better prepared for the future—whatever it may hold. Expanding the toolkit available to DC plan participants not only enhances retirement readiness but also aligns these plans with the broader evolution of institutional investment strategies.

Disclosure

This newsletter is limited to the dissemination of general information pertaining to Global Trust Company’s Trustee Services. As such nothing herein should be construed as the provision of personalized investment advice. The information contained herein is based upon certain assumptions, theories and principles that do not completely or accurately reflect your specific circumstances. Information presented herein is subject to change without notice and should not be considered as a solicitation to buy or sell any fund. Adhering to the assumptions, theories and principles serving the basis for the information contained herein should not be interpreted to provide a guarantee of future performance or a guarantee of achieving overall financial objectives. As investment returns, inflation, taxes and other economic conditions vary, the funds’ actual results may vary significantly. Furthermore, this newsletter contains certain forward-looking statements that indicate future possibilities. Due to known and unknown risks, other uncertainties and factors, actual results may differ materially from the expectations portrayed in such forward-looking statements. Readers are cautioned not to place undue reliance on forward-looking statements, which speak only as of a specific date. As such, there is no guarantee that the views and opinions expressed in this article will come to pass. This newsletter should not be construed to limit or otherwise restrict Global Trust Company’s investment decisions.

This newsletter contains information derived from third party sources. Although we believe these third-party sources to be reliable, we make no representations as to the accuracy or completeness of any information prepared by any unaffiliated third party incorporated herein, and take no responsibility, therefore. Some portions of this newsletter include the use of charts or graphs. These are intended as visual aids only, and in no way should any client or prospective client interpret these visual aids as a method by which investment decisions should be made. We have provided performance results of certain market indices for illustrative purposes only as it is not possible to directly invest in an index. Indices are unmanaged, hypothetical vehicles that serve as market indicators and do not account for the deduction of management fees or transaction costs generally associated with investable products, which otherwise have the effect of reducing the performance of an actual investment portfolio. It should not be assumed that the fund’s performance will correspond directly to any benchmark index. A description of each index is available from us upon request.